TRT-London asked me tonight about oil-market impacts of the deal between Iran and Oman. The title says most of it.

Of course there has been hardship globally with higher energy prices and volatility. However, compared to what would have happened 10 or 20 years ago, this is very significantly smaller.

Oil on average has been up only 25%, and refined products 36% since 28 Feb. (“Why Oil Prices Could Hit a Breaking Point by Year End,” WSJ, Video, 3aug26). Why?

The huge surplus in oil production that was building globally for at least three or four years, plus the constantly falling energy intensity of the economy, plus the high degree of interconnectedness of the one-global-barrel market (the name of this blog for the past 15 years) explains this relatively mild impact thus far. I explained this, and the geopolitical advantage, the long time line, it has given Trump and Washington to go slow and talk a lot as compared to the urgency they would have had earlier.

This is both a case of:

a) More oil being produced globally due to huge advances in petroleum and gas exploration and production (E&P) technologies, Especially in the USA, where a new “Fracking 4.0” stage of the Shale Revolution seems to be underway, one that could boost extraction rates of previously drilled wells by factors of 50-300%, according to various industry tech reports. This is all about US high tech and perfecting of methodologies. (See, Javier Blas, “Shale Oil’s Next Revolution Should Worry OPEC” Bloomberg, 30Nov25).

In addition, there have also been significant tech improvements in deeper offshore production, and in exploration generally, leading to a lot of new, large-sized proven reserves to exploit And,

Maxym Krapivnyy, host at Ukraine’s Kanal24 in Kyiv, spoke with me recently while I was in the USA about: Ukraine’s drone war vs. Russian energy, Russia’s economy, and the USA’s expanding energy war targeting Russia, Iran, Venezuela, and India’s Russian oil imports. I explained that soon, the late-Lindsey Graham’s (R, S.C.) and Richard Blumenthal’s (D., Conn.) “draconian” secondary sanctions bill is expected to be signed by Trump, blocking most Russian oil exports. (Note: the Senate yesterday voted 86-12, to advance the bill. See Blumenthal, here.)

However, Maxym also then asked my view on the likeliness of Putin soon agreeing to serious peace talks. I said I expected Russia would be unwilling to soon end the war even if its forces were pushed back to the Russian border. Why? To admit defeat would devastate Russian credibility as a Great Power in Eurasia and beyond. (See below for a comparison to the USA in Vietnam.)

On the energy war, I stressed that Russia is well known to be a petrostate. Russia’s wealth and capacity to finance aggression abroad overwhelmingly depends on its oil export revenues. Russia’s continued existence as a-petrostate is what the ongoing Ukrainian and USA energy offensives are targeting, on two main fronts.

There are two sides to this energy war. One is the Ukrainian’s kinetic war against Russia’s domestic refineries, the other is the USA and allies’ global sanctions offensive. Both aspects are evolving in breath and complexity:

First, there is the Ukrainian drone and missile campaign, including deep strikes against domestic Russian oil refineries and infrastructure. This has been gaining in success. I pointed out that these attacks have to, however, increase still more, requiting heavier missiles to close refineries and oil export terminal ports for sufficient time to render repairs unprofitable. However, Ukraine is now testing and has begun to produce such heavier weapons, which should be available in the short-to-medium term. We discussed Russia’s refined product supply problems, and what Ukraine must yet accomplish.

Second, oil which increasingly cannot be refined is pouring into Russian export terminals, its big Baltic and Black Sea oil ports. This was already the situation before the Iran war began on February 28. At that time, oil that could not be refined due to drone attacks was being loaded on ships for export. However, with USA sanctions having been intensified, many of these ships had no customers, it had nowhere to go. During the initial phase of the Iran war, the USA allowed India and other allies to purchase this oil (i.e., it unsanctioned oil already loaded on ships without any clear destination) to avert it going to China. This accumulation is apparently again building up, for the same reasons.

the USA now maintains sanctions against Russian oil firms Rosneft and Lukoil, and is working to supply India with non-Russian oil to end its Russian oil purchases, making it harder for Russia to find export markets besides China. However, the reclosing of Hormuz will of course make this somewhat easier for Russia to find buyers.

Two key themes here: Ukraine’s advances against Russia’s domestic oil infrastructure, and the Trump Administration’s global energy offensive, as shaping operations for a future conflict with China – or with the China-Russia-Iran axis. (Watch in Lithuanian) I told Aleksandra Ketlerienė, at Lithuanian national TV, that Ukraine is perhaps half way along in its kinetic capacities to forcing a collapse of a large part of domestic Russian refining capacities. (Interview in Lithuanian 14jul26).

I stressed that Ukrainian deep strikes in Russia must be taken as one side of a two-sided offensive vs. the Russian petrostate, with the other side being Washington’s targeting, logistics and other assistance to Ukraine’s air campaign, its harsh sanctions vs Rosneft and Lukoil, plus the announcement of a deal with Trump to impose the late-Senator Lindsey Graham (Rep., S. C.) and Sen. Richard Blumenthal’s (Dem. Conn.) self-described “draconian” secondary Russian sanctions, backed by about 93% of US senators, plus the US offensives vs. Iran and Venezuela focused on the oil-and-energy sector, and its continued work to pull India away from Russian oil — not as separate or chaotic events, but as part of a conscious, global energy offensive by the USA jointly with Ukraine and other allies, one which should be assessed as such, and not merely as individual, disjoint, haphazard “crises”. (On Ukrainian strategy, I cited its energy and intelligence expert, Mykhailo Gonchar, “From burning refineries to maritime blockade: a new strategy of pressure on Russia.” a valued colleague. 01jul26)

My assessment, since early 2026, has been that these should be understood as energy-sector “shaping operations.” That is, these are energy conflicts-of-choice aimed at optimizing the strategic post”ure of the USA and its allies to: destroy the petrostate basis of Russian power (see my EIES analytic paper, “Liquidating the Russian Petrostate, jan26), to secure allied access to Venezuelan (and Western Hemisphere-in-general) oil flows, and to Persian Gulf (Hormuz) oil flows in preparation for a kinetic conflict of whatever magnitude with China in the Indo-Pacific region. I should add that these energy “shaping operations” are intrinsic to the larger Trump administration strategy of “USA Energy Dominance” strategy, which I have discussed at GlobalBarrel.com.

NOTE – I believe it is important not to allow various sharp difficulties, setbacks or even failures that surely will occur on any of these fronts – vs. Russia, Iran and Hormuz, in Venezuela, with India, or directly with China – on the energy, and especially the oil front, to cause a loss of perspective that there is a global energy offensive or even a global energy war taking place, as a central part o the USA and de facto as part of the entire allied preparations (viz., as “shaping operations”) for a looming kinetic conflict with China and its allies – or, perhaps, is sufficiently successful, to dissuade China from aggression.

Also, recognizing the connected strategy is one thing, analyzing and critiquing the individual parts and overall rationale is another. For more, go to my blog at https://GlobalBarrel.com

Dr. Tom O’Donnell (for a keynote, consult or commissioned analysis for your organization, write twod(at)umich.edu )

I spoke with Kyiv Kanal24’s Nataly Lutsenko on three issues. Jump to a topic here: 1) Ukrainian drones in Russia 00:00:192) G7 push v Russian oil. 00:05:253) Who won the US-Iran war? 00:10:27 Recorded 18 June 2026.

Note on number 3: I said it is not yet clear who won the US-Iran war. This has to do with military capacities which the USA (and its allies) could bring to bear but are now deeply reluctant or unwilling to bring to bear.

If Iran is unwilling to compromise or, worse, plays games, as it has already in the past few days with its “Persian Gulf Strait Authority,” the USA might decide it is constrained to employ whatever means necessary (Carter Doctrine) to end the Islamic Republic’s capacity to restrict the free flow of energy from the Gulf.

Trump and USA officials understand that a full-on military option is not an optimal resolution. This led them to accept an MoU that is quite conciliatory to Tehran in order to get the Straight reopened, and also apparently in response to many of its Gulf allies unwillingness to absorb the punishment Iranian missiles and drones would inflict before the Straight is forcibly reopened and Iran’s missile capacities are eventually suppressed. The administration knows that a massive bombing campaign of the entire country’s military-industrial and civilian infrastructure, plus an occupation of the Iranian coast along the Straight could likely achieved their aims of removing the Straight from Iranian hegemony. However, this in turn, is likely to require a protracted force commitment to contain whatever regime forces remain active. No matter how minor, remaining missiles and drones, proxy forces and terrorist capacities could require a long time to resolve.

I explained that the price cap was de facto abandoned, replaced, by the Americans in 2025 with a campaign aimed at actually removing Russia’s capacity to export its seaborne oil. This campaign was de facto paused, first when they went after Venezuelan oil, and then during the war against Iran and the closure of the Straight of Hormuz.

However, the G7, including Trump, decided that they would focus again on pressuring Putin to end Russia’s war on Ukraine. Their decision was to focus now on sanctioning Russia’s oil and gas exports.

I explained how, just before Trump et al went after Maduro, in January, the Russian oil system had been pushed to the brink of a breakdown. This had been accomplished by a combination of the Ukrainian drone strikes deep inside Russia, particularly on oil infrastructure, a campaign conducted with detailed intelligence and targeting information provided by the USA, and by the imposition of sweeping new US sanctions Trump imposed on Rosneft and Lukoil and also by his having gotten Modi to agree that India would end the purchase of Russian oil. [See my study for EIES, Jan. 2026, “Liquidating the Russian Petrostate” or on GlobalBarrel.com]

One problem with giving a quick take on breaking news is that one can forget something. In the interview, I forgot about the US dollar swap line that the UAE had cajoled out of the USA –Trump and Bessent – just before it decided to quit OPEC. Below is the post I immediately wrote with many, IMHO, relevant issues underlying this move. These include national economic and geostrategic differences, often rather sharp, between the UAE and Saudis. However, the swap line issue is now included as point “Zero”.

-0.a- Regarding the swap line: there are so many pieces in motion that we need a litte overview refresher first.

As readers here know, my analysis is that the Trump administration’s sharp moves in the latter part of 2025 against Russian oil exports, together with the Ukrainians’ drone campaign, was at a point where it had begun threatening to force Russian oil exports offline. This, in turn, would force Russia to shut in its old and delicate West Siberian fields. I wrote a detailed study on this. This strategy is exactly like what the USA now openly says it intends to do to Iran by blocking exports from its Kharg Island oil terminal.

The Trump administration claims that the available Iranian storage on the island is near full (Scott Bessent has said this repeatedly). This will force wells to be shut in, likely ruining their productivity for the long term. (However, I believe the Iranian fields are not generally as fragile as Russia’s.)

-0.b- You will recall that Trump constrained and/or convinced India’s Modi to halt Russian oil imports as part of this larger anti-Russian oil campaign to press Putin to end the Ukraine war.

-0.c- However, before the USA proceeded to the next step vs. Russian exports, it went to Venezuela and took control of its oil sector, beginning a comprehensive and very rapid campaign there to bring Venezuelan oil back online.(I spoke at length to Swedish public radio on this again this week,)

The USA has shut off an approximately 2 million battels per day (mbd) stream of oil Venezuela was sending to China, and diverted that oil principally to India. That stream is now part of the USA effort to take care of India during the Iran crisis, so that it does not revert to taking Russian oil.

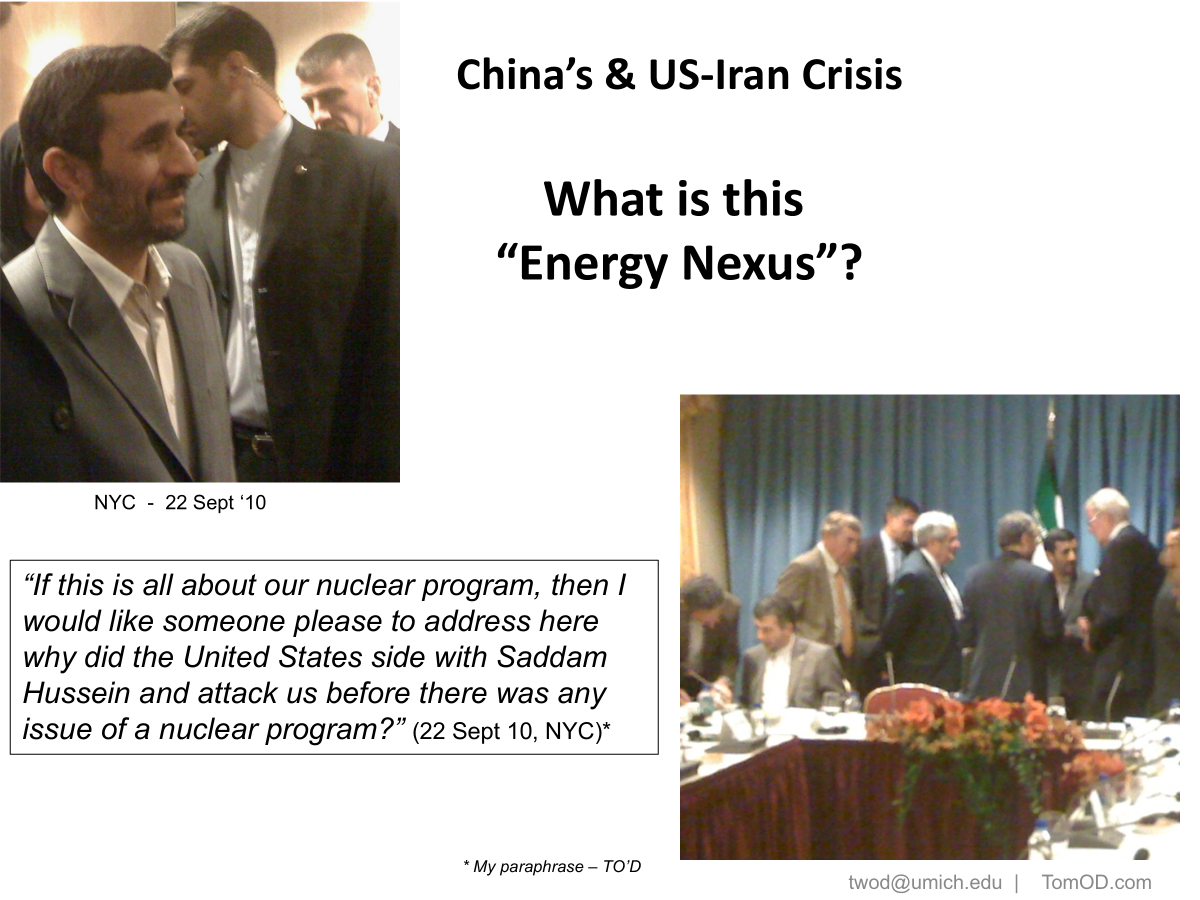

Pictures taken by the author (T.W.O’D) during a dinner and Q&A with President Ahmadinejad, in NYC during 2010 UN General Assembly opening. Note quote from Ahmadinejad.

Some years ago, I was invited to dinner with President Ahmadinejad in NYC during the annual opening of the General Assembly.

The American think-tanks, consultancies, and x-diplomats present went on and on asking detailed questions about this or that scenario where US experts might work with Iranian experts to observe or limit the Iranian nuclear enrichment program. (I mentioned this 2010 dinner in a later post: “China’s Iran-Oil Import Angst. Part I” Feb 13, 2012.)

It became rather tiresome. Ahmadinejad clearly was growing tired of it. He then asked us,

“If this is all about our nuclear program, then I would like someone please to address here why did the United States side with Saddam Hussein and attack us before there was any issue of a nuclear program?” (Iranian President M. Ahmadinejad, 22 Sept 10, NYC, my notes, T.O’D.)

Everyone ignored his question, and simply kept up with their obviously pre-prepared technical questions. But, what had he meant?

To me, clearly he was referring to the Iran-Iraq war (Sept.1980-Aug.1988), when the USA, at a certain point, decided to take Iraq’s side and, among other things, sunk the entire Iranian Navy in a day, took over air traffic control for the Iraqi air force, started directly advising Iraq on strategy, and etc.

In the end, Iran had to accept an Iraqi peace deal after a crushing defeat facilitated by the USA. I recall now all these details vividly. And, all this was indeed well before any nuclear program.

Aside: I find it disturbing that so many “experts” refer to the supposed “Iraqi defeat” in that war. This was all understood at the time. For example, I quote here from the NYT, (Sec. A, Page 1, of July 21, 1988): Ayatollah Khomeini had personally endorsed the cease-fire demanded by United Nations Security Council Resolution 598. Iran’s supreme religious leader confirmed, for the first time, that he had approved the resolution and added, with his characteristic rhetorical flair: ”Taking this decision was more deadly than taking poison. I submitted myself to God’s will and drank this drink for his satisfaction.” (Emphasis added to the most famous part of Khomeni’s statement. T.O’D.) Further research will quickly show he had to sign as Iran was being soundly defeated at the time, hence the “poison” he had to swallow.

By the way, it is also known, at least in academic circles, from later extensive archival research, that the war with Iraq was planned and instigated by Iran, and that Iraq had attacked in response to Iranian provocations and signs of Tehran’s preparations, after warnings. I am happy to send references to those interested.

What I myself had been arguing, back then, during the Iran-Iraq War Ahmadinejad was referring to, was that the US-Iran confrontation was actually about the US opposition to any country, either from inside the Gulf Region or outside the Region, gaining hegemony over the Gulf and the Straits of Hormuz. This had to do with guaranteeing the free flow of oil, and that the global oil market would be a “real” market that no one state could unduly control. I had even coined a term, “The Global Barrel,” for this market-centered, post-OPEC-nationalizations collective oil-security system, a system initiated by Henry Kissinger in 1973.

Guaranteeing Gulf energy flows to allies has always been a core US interest, while today’s Great Power Competition means China’s access will be rendered conditional.

This is not the Iraq war. If after operations to secure the coasts and islands and to clear mines, the Iranian regime resists, the USA plan is that Iran’s oil sector and economy would be destroyed by aerial bombardment. Washington neither desires nor needs to occupy Iran proper nor to change the regime. The US strategic imperative here is to secure, long term energy flows from the Region and, accordingly, to end the regime’s capacities to project regional power.

After almost 30 years of analysis and my university seminars, there is very little I see new here, save a new USA urgency.

In my view, this urgency flows from USA concerns over Great Power Competition, especially with China. This is exacerbated by the possibility that Iran could close the Strait in solidarity with China (or perhaps Russia) during any Great Power conflict elsewhere. The threat of Iran’s developing capacities in this regard, especially its missiles and drones, but also its nuclear weapons ambitions and intentions to rebuild its regional proxy allies, all act to undermine the prerogatives of the USA and its Gulf regional allies to secure the region and its energy flows.

In any case, the idea that Washington and Trump “have no strategy” is demonstratively wrong, and self-disarming. (See, for example, my EIES study of Trump administration energy policy since ca. April 2025 v. Russian oil.) One might not fully understand the strategy, or might disagree with it, but there is clearly a multifaceted strategy here under the general slogan of “USA Energy Dominance” (e.g., see posts here and here). Besides Iran, it especially includes Russia, Venezuela, India, and of course China, as well as US domestic oil, gas, nuclear and renewables policies.

Author’s screen shot from NTD News. The statement was posted on Tuesday.

Note, a third Amphibious Assault Group, an aircraft carrier with an additional Marine Expeditionary Unit of 2000-2500 troops, has just arrived to join two other already in the Region. This further shows that Trump is increasing preparations to seize Hormuz, not backing down.

Yet, tragically, even Merz’s conservatives-in-power still profess faith in 100% renewables “eventually” & nuclear “never” … despite deindustrialization.

The title above says it all. I pointed out that Germany produced about half its electricity from renewables in 2025 such as wind and solar.

However, more renewables have only caused prices to soar, and helped to drive German deindustrialization.. Much of the rest of the EU has similar problems from over-installation of renewables (Note: I coined the term “Renewables Fundamentalism” to describe this), as a Green panacea for both climate change mitigation and supposed energy independence. Aside from the high complexity of integrating ever more renewables that are highly-distributed (spread out over large land masses) and hard to integrate (requiring complete rebuilds and extensions of grids), while the problems of their unreliability (variability, depends on wind speed and amount of sunshine), is their Achilles Heel.

As I told Al Jazeera in this brief interview, once a country has over about 25% dependence on renewables, it requires a complete and highly expensive total rebuild of their grids, and a system of alternative-to-renewable generation in periods of low wind and solar, which the Germans call Dunkelflaute.

Both Christof Rühl (bio) and Jack Kemp (bio) had great, data-driven media this past week. I too addressed these issues (spoiler: I assess Trump is not bluffing on Iran talks, and oil supply remains adequate.) My conflict-trajectory take differs a bit from Chrisof, perhaps closer to Jack K here.. My Al Jazeera was just after Trump announced talks.

Dear readers, This paper, which I wrote in 2008-09, analyzed the evolution of interests underlying the US-Iran crisis till then, interests which persist in the 2026 US-Iran war.

That is, Trump’s “USA Energy Dominance” strategy does not seek to fundamentally alter the structure or logic of the post-1973 global, market-centered, USA-led-and-protected oil order. However, to preserve it, the USA now feels the necessity of removing the Iranian mullahs as custodians of Iran’s oil for persistently insisting on projecting power and seeking hegemony in the energy-critical Gulf Region.

What is new from 2008, is the bipartisan urgency felt in Washington to renovate the existing oil market-and-security order, reconsolidating the USA as primary arbiter of energy flows via Hormuz to both China and US allied and friendly states of the Indo-Pacific region. In addition, to be capable of significantly blocking Russian oil exports and thereby its petrostate-fueled aggression elsewhere.

In particular, it mush achieve these aims, vis-a-vis Russia and China, without causing global oil shocks. (continued in full-column below …)

Mar 12, 2026. Is the Iran war about the US containing China? For my part, I explained how control of Hormuz would give the US two key levers:

The USA will control half of China’s oil imports, 5.4 million barrels per day (mbd), which flow through Hormuz.

The USA will insure that during any Pacific war China might start that Iran, acting in solidarity with China, could not block oil flows to US Asian allies such as Japan, S. Korea, Australia, Philippines, or flows to others whose supplies it would also want to guarantee, such as Viet Nam, Indonesia, Malaysia, Singapore, etc..

I was a bit insistent that the spike during the day today, to over $100 at some point, was overblown.

As I mentioned, Fatih Birol at IEA (I forgot to mention also Chris Wright, USA Secretary of Energy),who had said the same thing, insisting last Friday that there is plenty of oil in the market. (See Wright and Bloomberg’s Steven Stapczynski elaborate here). That is NOT a problem now.

And, in the interview, I detailed some facts about this (e.g., before the war started nine days ago, there were about 1.4 billion(!) barrels floating on the water, an unprecedented amount, and the Russians had nowhere to put their unsellable oil).

So, It turns out that late Monday evening news (EST USA time), the news coming from the USA vindicates my suspicions. For now, there is no plan by the administration to release SPR reserves into the market.

Notice what I explained about this likely being a short-lived boost for Russian oil That is, after the Venezuelan campaign, if the Trump admin. Iran campaign works, both China and Russia will be in a very restricted position in the now-USA tightly controlled international oil market supply chain.

Here is the WSJ saying the prices of oil dropped quite a bit, and the stock market rebounded as well by the end of the day. Following that is a Bloomberg take too.

This is a longish, ca. 30 minute video. Host Nataly Lutsenko kindly told me she wanted to make a long interview.

(During time of crisis like this, I have so many TV and press interviews that I don’t have time to put most of them online. So, I will refrain from writing long posts to accompany videos to get more online, if I think they are useful interviews. – Tom O’D)

Last night on TRT World Global News (London), I emphasized that despite the modest spike in oil prices from about $70 to $78 per barrel as of yesterday, Trump has an historically unprecedented advantage for exercising “US Energy Dominance.”

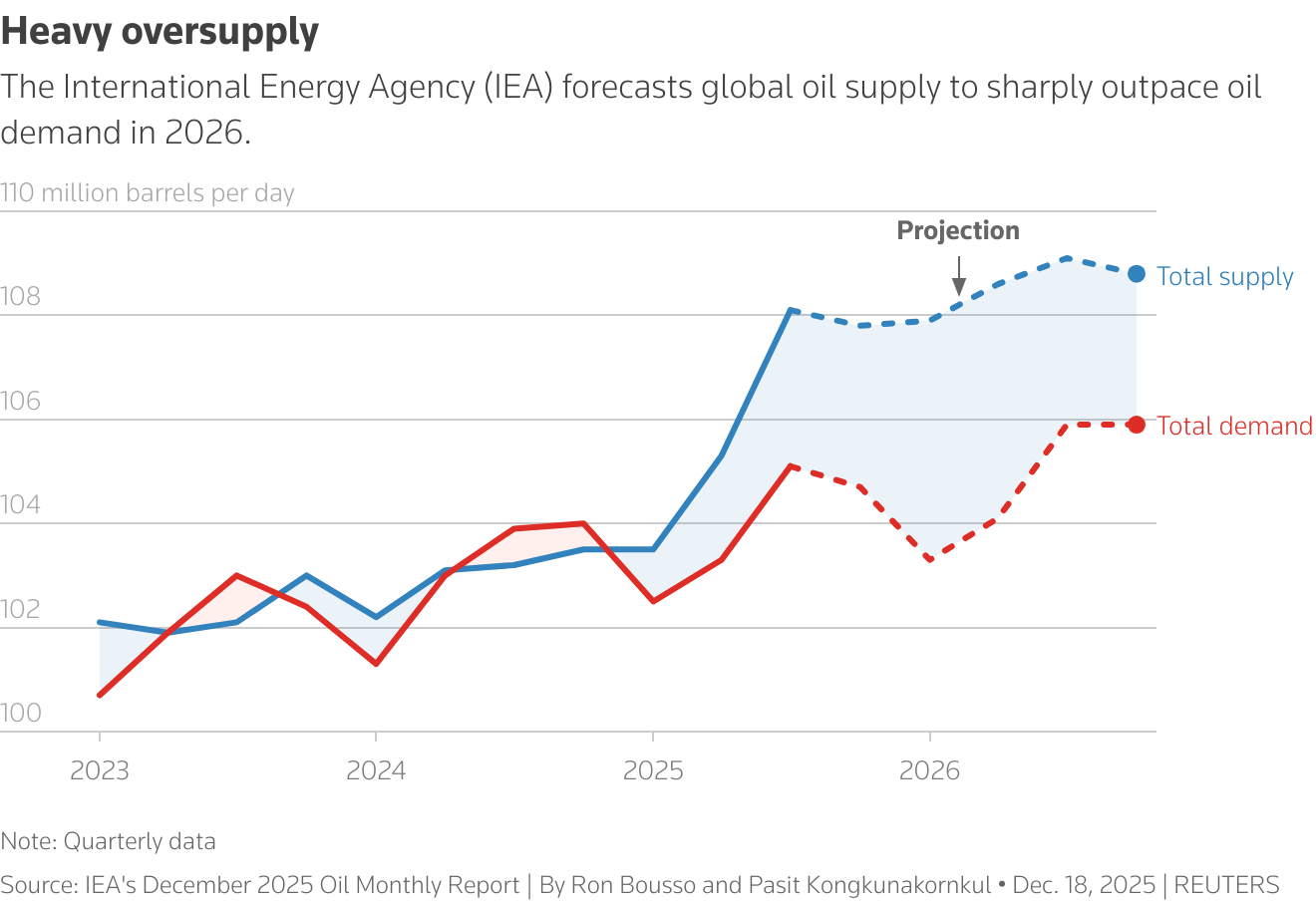

Fig. 1. IEA projects global oil glut throughout 202

The campaigns against Venezuela and Iran, plus the turning of the Indian oil-consuming behemoth towards USA and Western interests vs Russian oil, are examples of the geopolitical leverage the USA’s now-dominant role in global oil affairs has afforded the Trump administration.

This oil-market advantage comes mainly from of two things: