Last night on TRT World Global News (London), I emphasized that despite the modest spike in oil prices from about $70 to $78 per barrel as of yesterday, Trump has an historically unprecedented advantage for exercising “US Energy Dominance.”

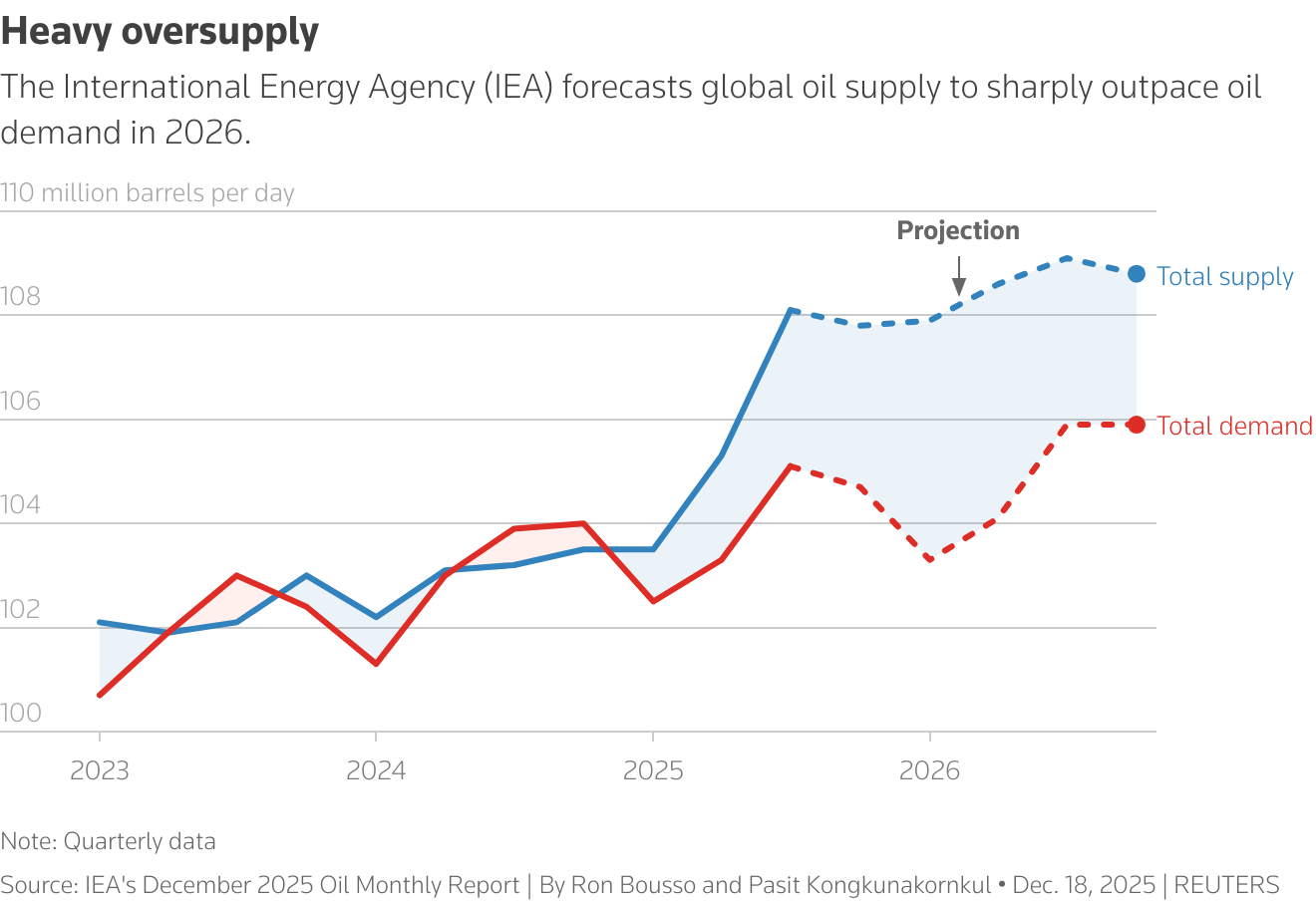

Fig. 1. IEA projects global oil glut throughout 202

The campaigns against Venezuela and Iran, plus the turning of the Indian oil-consuming behemoth towards USA and Western interests vs Russian oil, are examples of the geopolitical leverage the USA’s now-dominant role in global oil affairs has afforded the Trump administration.

This oil-market advantage comes mainly from of two things:

I discussed with Artur Ciechanowicz (BizNesAlert.pl) how Chancellor Merz and Energy Minister Reiche refuse the one reform that can really boost German energy security: focusing on nuclear energy as France has, and Poland has begun to do. (Read below in English or in Polish) — Twice last week, Merz indicated willingness to work with Russia when the Ukraine war ends. For two decades before the war, working with Russia meant more Russian gas imports, building Nord Stream 1 & 2. Now Merz worries about dependence on USA LNG. However, the German model he continues, one of installing BOTH a full-scale, wildly complex renewables system, plus a full-scale natural-gas backup system, guarantees high-cost energy, deindustrialization and foreign energy dependence.(Polish at BizNesAlert.pl)

Amerykański ekspert: Niemcy znów myślą o gazie z Rosji

Wcześniej czy później Niemcy ponownie będą racjonalizować podporządkowanie się Gazpromowi Putina w imię +dywersyfikacji+ dostaw – ocenia Thomas O’Donnell, ekspert ds. energii i geopolityki z amerykańskiego think-tanku Wilson Center. Na zdjęciu kanclerz Niemiec Friedrich Merz.FOTO: x.com/_FriedrichMerz

Berlin zaczyna zmieniać kurs wobec Rosji i znów będzie racjonalizować współpracę z Putinem w imię „dywersyfikacji” dostaw gazu. Stanie się tak, bo Niemcy nadal opierają swoją strategię energetyczną na OZE wspierane gazem, zamiast postawić na atom jako priorytet – ocenia w rozmowie z Biznes Alert amerykański ekspert Thomas O’Donnell.

Wypowiedzi kanclerza Niemiec Friedricha Merza o potrzebie „pojednania” z Rosją, wygłoszone dwukrotnie nie da się traktować, jako wyrwanych z kontekstu i przypadkowych. To sygnał polityczny. Najbogatsze państwo Europy i przemysłowy motor Unii Europejskiej zaczyna rewidować swoją linię wobec Moskwy.

Merz z ufnością o Rosji

– Jeśli uda nam się przywrócić pokój i wolność w Europie, jeśli ponownie odnajdziemy równowagę w relacjach z naszym największym europejskim sąsiadem, czyli z Rosją, jeśli zapanuje pokój i zostanie zapewniona wolność – jeśli to wszystko nam się powiedzie, wtedy Unia Europejska, a wraz z nią my w Niemczech, przejdziemy kolejny test i będziemy mogli z ufnością patrzeć w przyszłość także po 2026 roku – powiedział szef niemieckiego rządu na spotkaniu noworocznym z przedstawicielami przemysłu i handlu 14 stycznia w Halle, dodając potem: „(…) jeśli w dłuższej perspektywie uda nam się na nowo przywrócić równowagę w relacjach z Rosją, gdy zapanuje pokój i gdy wolność będzie zagwarantowana”.

Niemiecki przemysł od 2023 roku zmaga się z wysokimi cenami energii, spadkiem konkurencyjności, rosnącą presją chińskich producentów oraz stagnacją wzrostu gospodarczego. W 2024 roku niemiecka gospodarka formalnie weszła w recesję techniczną, a prognozy wzrostu na 2025 rok były jednymi z najsłabszych w UE.

Wypowiedzi Merza nie oznaczają natychmiastowego zwrotu w polityce wobec Moskwy ani propozycji zniesienia sankcji. Nie są ofertą pokoju ani jednostronnym gestem. Wskazują jednak na rosnące przekonanie w niemieckich elitach politycznych i gospodarczych, że obecny stan konfrontacji – bez realistycznej strategii wyjścia – osiągnął dla nich próg bólu.

„Powrót do „mafijnego bossa od gazu”

Thomas O’Donnell, ekspert ds. energii i geopolityki z amerykańskiego think-tanku Wilson Center wyjaśnia w rozmowie z Biznes Alertem intencje Merza: „Niemieckiemu kanclerzowi chodzi przede wszystkim o uniezależnienie się od pełnego sojuszu z USA, od zależności od Stanów Zjednoczonych. Jednak powrót do starego +mafijnego bossa od gazu+, Władimira Putina, trudno nazwać niezależną strategią”.

Z analizowanych przez O’Donnella wypowiedzi i komentarzy, a także z poufnych rozmów wynika, że niemieccy urzędnicy rządowi traktują amerykańską energię, jako potencjalnie równie zawodną jak tę z Rosji.

– Merz zlecił w związku z tym swoim ludziom znalezienie rozwiązań. Oczywiście, metody Donalda Trumpa w relacjach z sojusznikami nie są konstruktywne. Mimo że Niemcy są teraz ogromnym odbiorcą LNG z USA, to amerykański prezydent traktuje te biznesowe więzi również jako instrument nacisku – zaznacza ekspert.

– Jednak źródło problemu leży w nierealistycznej polityce energetycznej ostatnich czterech kanclerzy. Merz dostrzega problem silnie subsydiowanych odnawialnych źródeł energii oraz nadmiernej zależności od rosyjskiego gazu. Ale wciąż nie widzi, że Niemcy nie mogą zapewnić sobie bezpieczeństwa energetycznego ani przystępnych cen, opierając się na zależnych od pogody OZE wspieranych gazem. Postawienie na nową energetykę jądrową jako priorytet to jedyna droga — co Francja jasno udowodniła – dodaje.

Niemcy znowu pomyślą o gazie z Rosji

O’Donnell zwraca uwagę, że Merz i jego rząd popierają kontynuację budowy tych samych dwóch równoległych systemów, które tworzyli poprzedni dwaj kanclerze: jednego opartego wyłącznie na OZE i drugiego — gazowego — jako zaplecza na dni bez wiatru lub słońca.

– W praktyce tak zwana reforma polityki energetycznej Merza polega na tym, że dalsza rozbudowa OZE i sieci ma być teraz w większym zakresie finansowana z prywatnych środków, a planowane ogromne instalacje turbin gazowych również mają powstać — tyle że zasilane LNG z USA, a nie rosyjskim gazem – podkreśla Thomas O’Donnell i ocenia, że nie jest to radykalna, strukturalna reforma energetyczno‑przemysłowa, której Niemcy potrzebują, a jedynie kosmetyczna zmiana.

– W sposób konieczny wcześniej czy później doprowadzi to do tego, że Niemcy ponownie będą racjonalizować podporządkowanie się Gazpromowi Putina w imię +dywersyfikacji+ dostaw. Czy to z powodu ideologiczno‑technologiczno‑politycznego zamieszania, czy oportunizmu — niemieccy przywódcy nie dostrzegają, że już istniejące OZE i każda nowa generacja gazowa powinny być traktowane jedynie jako rozwiązania pomostowe, podczas gdy rozwój energetyki jądrowej powinien być priorytetem – jako jedyna realna droga – podsumowuje amerykański ekspert.

Artur Ciechanowicz

American expert: Germany is considering gas from Russia again

Sooner or later, Germany will once again rationalize its subordination to Putin’s Gazprom in the name of “diversification” of supplies, says Thomas O’Donnell, an energy and geopolitics expert at the American think tank Wilson Center. Pictured is German Chancellor Friedrich Merz. PHOTO: x.com/_FriedrichMerz

Berlin is beginning to change course towards Russia and will once again rationalize cooperation with Putin in the name of “diversifying” gas supplies. This will happen because Germany continues to base its energy strategy on renewable energy supported by gas, instead of prioritizing nuclear power, American expert Thomas O’Donnell told Biznes Alert.

German Chancellor Friedrich Merz’s statements about the need for “reconciliation” with Russia, made twice, cannot be dismissed as out of context or coincidental. They are a political signal. Europe’s richest country and the industrial engine of the European Union is beginning to reconsider its stance towards Moscow.

Merz with confidence about Russia

– If we manage to restore peace and freedom in Europe, if we manage to find balance again in relations with our largest European neighbor, Russia, if peace prevails and freedom is guaranteed – if all this succeeds, then the European Union, and with it we in Germany, will have passed another test and will be able to look to the future with confidence even after 2026 – said the head of the German government at a New Year’s meeting with representatives of industry and trade on January 14 in Halle, later adding: “(…) if in the long term we manage to restore balance again in relations with Russia, when peace prevails and freedom is guaranteed.”

German industry has been struggling with high energy prices, declining competitiveness, increasing pressure from Chinese manufacturers, and stagnant economic growth since 2023. In 2024, the German economy formally entered a technical recession, and growth forecasts for 2025 were among the weakest in the EU.

Merz’s statements do not signal an immediate shift in policy toward Moscow or a proposal to lift sanctions . They are not an offer of peace or a unilateral gesture. However, they indicate a growing conviction among German political and economic elites that the current state of confrontation—without a realistic exit strategy—has reached their pain threshold.

“Return to the ‘Mafia Gas Boss'”

Thomas O’Donnell, an energy and geopolitics expert from the American think-tank Wilson Center, explains Merz’s intentions in an interview with Biznes Alert: “The German chancellor is primarily concerned with becoming independent from a full alliance with the United States, from dependence on the United States. However, returning to the old ‘mafia gas boss’, Vladimir Putin, is hardly an independent strategy.”

Statements and comments analyzed by O’Donnell, as well as confidential conversations, indicate that German government officials view American energy as potentially as unreliable as that from Russia.

“Merz has therefore tasked his people with finding solutions. Of course, Donald Trump’s methods in relations with allies are not constructive. Even though Germany is now a huge recipient of LNG from the US, the American president also uses these business ties as a tool for pressure,” the expert notes.

“However, the root of the problem lies in the unrealistic energy policies of the last four chancellors. Merz recognizes the problem of heavily subsidized renewable energy sources and excessive dependence on Russian gas. But he still fails to see that Germany cannot ensure energy security and affordable prices by relying on weather-dependent renewable energy sources supported by gas. Prioritizing new nuclear energy is the only way forward—as France has clearly demonstrated,” he adds.

Germany will think about gas from Russia again

O’Donnell points out that Merz and his government support the continuation of the construction of the same two parallel systems that the previous two chancellors created: one based solely on renewable energy and the other – gas – as a backup for days without wind or sun.

– In practice, the so-called Merz energy policy reform means that further expansion of renewable energy sources and the grid is now to be financed to a greater extent from private funds, and the planned huge gas turbine installations are also to be built – but powered by LNG from the USA, not Russian gas – emphasizes Thomas O’Donnell, assessing that this is not the radical, structural energy and industrial reform that Germany needs, but merely a cosmetic change.

“Sooner or later, this will inevitably lead to Germany once again rationalizing its subordination to Putin’s Gazprom in the name of ‘diversification’ of supplies. Whether due to ideological, technological, and political confusion or opportunism, German leaders fail to recognize that existing renewable energy sources and any new gas-fired generation should be treated merely as bridge solutions, while the development of nuclear energy should be a priority—the only viable path,” the American expert concludes.

My comments are linked here:: -1- 02:21, -2- 06:52 -3- 14:30 -4- 20:50, but hear Aura & Oktay too!

I was happy to address Türkiye’s push to become a gas hub: both for its own domestic security of supply, and to become an indispensable supplier to the European market. I was on with esteemed gas-sector analysts Aura Sabadus and Oktay TanriseverI, and host Yusuf Erim. TRT is a state-supported Turkish national broadcaster. The Turkish, East Med, Central Asian, Caspian regions involved are fairly complex, and I will simply let the interview speak for itself. Turkey is making progress but needs to end market-price setting, as Aura Sabadus stressed – and I agreed, as well as further diversification of supplies. I stressed the self-destructive EU lack of interest in long-term new pipeline gas from Azerbaijan and Turkmenistan it could indeed contract for, which would all transit Turkey.

You will see (my 3rd answer) that I raised again my view that Europe will become ever more deeply in need (i.e., dependent) on natural gas imports, but is acting rather “schizophrenic” about this. Brussels et al seems not to be willing to face this reality. Natural gas importance and its geostrategic nature will only increase due, perhaps counter-intuitively, to EU over-dependence on renewables. But, where is the urgency, then, to sign long-term pipeline-gas contracts from neighboring states via a developing Turkish gas-sales hub? Such supplies would generally be cheaper than LNG imports, especially if the LNG is purchased on short-term spot markets. Indeed, even its main pipeline supplies now, from Norway, are reportedly mainly via short-term spot purchases (See Morten Frisch, Norwegian gas-sector veteran). I find this astonishing for both price and security of supply.

Here’s my interview and a written elaboration – in lieu of a transcript:

Trump’s “tariff shock” on everyone was intended mainly to force negotiations. Especially this is to insure no country:

Functions as a transit state for Chinese exports to get into the USA without paying crippling tariffs, or

Provides a Chinese-owned manufacturing site in their country with the same aim of accessing the USA market without crippling tariffs..

Trump’s Chair of the Council of Economic Advisers Miran and Treasury Secretary Bessent have been fairly clear about this, if one listens in detail.

Trump Tariffs’ impact on Europe – Deindustrialization. German auto sector as an example.

While Trump and his circle militate against “deindustrialization” of the USA accomplished over the past few decades by the growth of Chinese manufacturing capacity and the export of these products into the USA market, Europe has an immediate problem, however, with the current advance of its “deindustrialization” or, as some more optimistically say, its new industrial “evolution”. [Some references from major German economic institutes on deindustrialization: IFO Institute, IW Institute, Kiel Institute, the latter of which has evolved a bit on this].

Taking the German auto industry as an example, it was already suffering from well known, chronic problems of Germany’s own making. These include two decades of low infrastructure investments, poor digitalization, high taxes, and being subjected to arbitrary government mandates to reduce diesel sales and increase battery electric vehicle production, and etc. ON top of this, German industry has also suffered high energy prices due to the countries exceptionally complex all-renewables energy transition model. On top of this came suddenly, from 2021, the Russian energy war, which denied Europe half of the cheap gas that European, and especially German industry was relying on to compensate for the high-cost of the all-renewables transition.

This energy war – and on the heels of the Covid shock – was devastating to German manufacturing and heavy industries, providing the proverbial straw that broke the camel’s back. In my assessment at the time, this was the point at which German industry’s problems of multi-faceted uncompetitiveness morphed into a form of deindustrialization,

Germany is in its third year of recession. However, this is not just a recession. Note that the VW, the German auto firm, for example, in September 2024, began mass layoffs for the first time in 87 years in September 2024. BASF is in a similar conundrum. In my view this is a systemic, secular problem over and above any present economic downturn.

So, the point of painting this detailed picture of the crisis of German automobile manufacturing, as an example, is that one can now really only imagine what a sharp knock-on effect Trump’s auto tariffs and his other tariffs might have on top of all this. This is devastating. Already the CEO of Mercedes has said if the tariffs continue he will move the production of the cheaper models to the USA. Already one of the largest exporters of cats from the USA is a German factory.

My response (critique) of Jeff Sacks‘ dollar-decline predictions

I was asked to listen to a clip from Asharq/Bloomberg’s earlier on-air interview with Nobel Prize economist, Jeffry Sachs, about his prediction that the US dollar would lose its reserve currency status in this decade and be replaced by regional currencies.

My take was that there was little new (or old) factual evidence of this, plus Trump’s tariff shock is not necessarily a long-term tactic. So, I commented that Sachs has had this theory for a long time, an it is nothing new. (I think it is fair to say he is quite sympathetic to China in various interviews, for some years now.) So, I simply said I was not surprised he says this, as he has for a long time.

However, I explained (with a bit more factual detail than Sachs, I hope) that indeed, even Trump’s theorist Miran and Bessent too agree that the tariffs strategy is designed to reduce the value of the dollar (its aims is precisely a weak dollar), and this should normally mean that the dollar loses its reserve currency status, its preferred use in the world, that these Trump theorists have a plan for a “Mar-a-Lago” or similar accord for states that are seen as being key, close allies, who would agree to peg their currencies to the dollar, and that they should be expected to agree as they need to trade into the USA market.. This is based on the observation that the USA market has a special status in the world. If this were to pass, they theorize that this would in fact preserve the special, preferred reserve status of the US dollar. Trump likes this as he has said that if this status is lost, then the destiny of the USA is to be a “third world” economy. **Continued at GlobalBarrel.com ….

I felt greatly honored to speak in Ireland, the home of my ancestors, at a high-level Irish-Polish event, invited by the Polish embassy as part of Poland’s Presidency of the European Council. [Spoiler alert: my assessment of the Green Deal’s impact on EU energy security and competitiveness was highly critical. And, I called for a radical reform, modeled on the 1970-80’s French Messmer nuclear program, the response to a similarly dire European energy and competitiveness crisis.]

For Ireland we had Secretary General Oonagh Buckley and Wind Energy Ireland CEO Noel Cunniffee; for Poland, Daniel Piekarsky, Head of Energy Security Unit in the Foreign Ministry, and myself, Global Fellow of the Wilson Center, Washington (external) working in Europe, from Berlin.

Our moderator, from the Polish Embassy, Dublin, was the Polish diplomat and patriot, Dr. Jacek Rosa — a good friend, with whom I had the great pleasure of closely collaborating, for several years, in opposition to the Russian-German Nord Stream 2 gas-pipeline partnership, before the 2022 full-scale invasion of Ukraine. Below is the lineup, the initial invitation and some pictures. The event was off-the-record, so I show here only my own, slightly redacted talk.

Opening of Nord Stream1 pipeline, 2011. Gazprom via PAP

Below are links to 12 articles that appeared in the Polish press in the last few months, interviewing or quoting me on four topics I feel are important. The topics are listed in the title above.

The links are below, sorted by topic. The first or left column has English translations of the titles, and the second or right column has the original Polish — which unfortunately I don’t speak! If you follow the links, Google Translate or Deepl will translated the Polish articles pretty well into English. My special thanks to the intrepid Polish journalist, Artur Ciechanowicz at BiznesAlert in Warsaw for his interviews in the list. (I also had about 33 quotes or interviews in several other languages since December [1]).

ENGLISH titles and links:

On German (far-right) & USA (Trump) each plotting a Russian gas return to Germany

A former Stasi agent lobbies for the resumption of Nord Stream. Expert: One of the gas pipeline lines ready to be launched,, By,:Artur Ciechanowicz, March 3, 2025, biznesAlert.pl

Some EU countries believed that Gazprom gas would be in Europe forever BiznesAlert.pl

“Like a Drug Addict Returning to Heroin.” Analyst on the Idea of Unblocking Gas Imports from Russia to Europe, Author: Artur Ciechanowicz, February 1, 2025, 07:21

Failures of EU Green Deal on technology and energy security.

American expert: recommendation to reduce emissions by 90 percent by 2040 is “fantasy” | Energetyka24

Expert: EC recommendation to reduce gas emissions is fantasy wpolityce.pl

Unrealistic EU climate plan. Expert opinion crushes – Super Business

“Rearranging deckchairs on the sinking Titanic”. Expert slams the eco-target dictates of Brussels Eurocrats – PCH24.pl

Trump, EU & Poland: Ukraine War crisis.

First talk with Putin. Trump has visions of ending the war in Ukraine | Newsweek Jan 21

How Trump Can Bring Down the Russian Economy: Analysts: He Has an Arsenal of Means to Do It, By Artur Ciechanowicz, Jan 24, 2025 | Biznes Alert

Trump may use [oil] sanctions to finish off Moscow, which is running out of money for the National Welfare Fund. – 16 January 2026 UBN

Expert: Washington, London, Warsaw should work quickly. Kiev can’t afford to be patient – Dziennik.pl

German deindustrialization: Energy & economic crisis

Major shoe retailer goes bankrupt A sharp increase in bankruptcies in Germany

Polish titles and links:

First topic.

Agent Stasi lobbuje za wznowieniem Nord Stream. Ekspert: Jedna z nitek gazociągu gotowa do uruchomienia biznesalert.pl

Część krajów Unii uwierzyła, że gaz z Gazpromu będzie w Europie na zawsze BiznesAlert.pl

“Jak powrót narkomana do heroiny”. Analityk o pomyśle odblokowania importu gazu z Rosji do Europy | BizNes Alert

2nd Topic

Amerykański ekspert: zalecenie redukcji emisji o 90 proc. do 2040 r. to „fantastyka” | Energetyka24

Ekspert: Zalecenie KE redukcji emisji gazów to fantastyka wpolityce.pl

Nierealny plan klimatyczny UE. Opinia eksperta miażdży – Super Business

“Przestawianie leżaków na tonącym Titanicu”. Ekspert nie zostawia suchej nitki na eko-dyktaturze brukselskich eurokratów – PCH24.pl

Third topic

Donald Trump chce uchronić świat przed III wojną światową | Newsweek

Jak Trump może złamać rosyjską gospodarkę?

Trump may use [oil] sanctions to finish off Moscow, which is running out of money for the National Welfare Fund. – UBN

Ekspert: Waszyngton, Londyn, Warszawa powinny szybko działać. Kijowa nie stać na cierpliwość – Dziennik.pl

[1] Other than being cited/interviewed in Poland, I was also quoted elsewhere about 33 times so far in 2025, mainly in the USA, with many then translated to languages of Europe, Asia and Latin America. I never know what to do with all these print interviews. Here at GlobalBarrel.com, I often publish videos of some of my live-on-air expert commentary, usually accompanied by a detailed blog post. So, my idea is I will make a new tab at the top of the GlobalBarrel.com site, next to the “About Me” tab, where I can simply list link to my recent press citations or Op-Eds. [Back to text]

10-12 February, I was invited to contribute to the NATO Advanced Research Workshop (ARW) on critical European infrastructure, organized in Podgorica by the Atlantic Council of Montenegro, a NATO member, and The International Society for Risk Management (ISRM), Serbia, a non-NATO member. This partnership plus experts from neighboring states made the workshop on risks to regional and West Balkan infrastructure very informative. I felt quite honored, as a regional outsider, an American working on EU energy and geosecurity (based in Berlin), to be invited. Conference FB link

I planned to discuss drivers of EU deindustrialization, but decided to focus on one sharp example: how tech failures in the EU’s energy-infrastructure model, the Green Deal, is causing the unexpected 2025 EU natural gas crisis. This comes while gas prices were still high and supply still problematic from the 2022-23 Energy War – caused by Russia maliciously stopping Nord Stream pipeline flows. This new hit to European competitiveness and security was, however, an eminently avoidable “own goal.” (The workshop discussion is off the record, but I may post my own talk.)

How has the Green Deal model caused another gas crisis?

The EU Green Deal model requires installation of high percentages of wind and solar renewables. However, to supply energy reliably, installation of wind and solar renewable (RE) technology must be paired with installation of sufficient universal, long-term, grid-scale storage (ULTGSS) technology. The idea is excess electricity generated on very sunny, windy and mild days should be stored to compensate supply on dark, calm and cold days. (Let’s put aside, for now, expert debunking of this RE-plus-storage model using weather and tech data.) Over-installation of solar and wind beyond what can be backed up by some other source, is a critical vulnerability to energy infrastructure reliability during periods of cloudy, calm and cold weather. This is called “Dunkelflaute” in German.

However, the reality is that, after some four decades of storage-tech R&D, such a technology still does not exist. There is no lack of studies and data on this. However, EU members remain mandated by the Green Deal and ancillary EU and/or national laws to continue installing ever higher percentages of renewable generation.

As a result, Dunkelflaute conditions in late-November and early December 2024, and again in February 2025 across northern Europe led to prolonged periods of plunging RE generation. Without the aforementioned ULTGSS backup (my acronym), the “de facto ULTGSS” has primarily been natural-gas-fueled generation, plus importing of nuclear, hydro and coal generation from neighboring countries having excess capacity in these.

My talk was an analysis the root cause for another EU natural gas crisis this winter. I explained that the EU’s initial win in the energy war imposed on it by Putin, overcoming the initial, acute crisis of 2022, is nevertheless evolving dangerously into a Pyrrhic victory – into a defeat. This is because EU energy policy, the Green Deal, has critical technological failings, and the present EU Commission leadership refuses to reform it, rejects any serious criticism of the model, and is instead doubling down on an all-renewables system ASAP. In fact, it is assumed that Van der Leyen will announce, late in February, adoption of a new, more “ambitious” target of 90% net-zero emissions by 2040 relative to 1990. (GlobalBarrel.com readers might recall I termed this as “fantasy” in Op-Eds last year in the Polish daily press and elsewhere.)

A Green Deal reform, based on science, is not inherently “right”, “center” or “left”

I explained why a radical reform of this Green Deal model should not be a matter of political philosophy, rather ait requires only an honest recognition that the tech simply does not exist for this scale of installations. Refusal to reform is no longer only anti-science Green populism. After ca. 15 years of this Green Model’s hegemony in various member states, then in Brussels, ALL PARTIES are beset with ideological-scientific confusion and need a certain fresh start, a reeducation or green-energy deprogramming. In particular, center-right parties, such as the CDU in Germany, are typically confused in that they tend to see the entire problem as one of the methods of financing the Green Deal (and the German Energiewende, which provided the model the Green Deal is based on). They focus on having less government mandates, less subsidies, more public financing, and a more liberal, interconnected electricity market in Europe. All well and fine. However, if one is talking about alchemy, funding the transmutation of lead into gold, then it matters little how efficiently it is financed, and how liberal is the market model. In this case, the problem is that a highly RE based model (much less the German, Spanish, Austrian, etc. model of 100% renewables), lacking any universally applicable, long-term, grid-scale storage, is simply energy-infrastructure “alchemy”. It is simply impossible without an entire parallel natural gas system on standby awaiting any instance of Dunkelfloute. This is a disaster, an impossibly complex and expensive model that guarantees ever deeper EU deindustrialization.

Even the farthest right and left parties are hesitant to embrace a fundamentally different model of massive large-scale nuclear as the basis, with also extensive electricity-fueled mass transit build-outs as a clearly already-proven model. The alternative is further high energy prices, deindustrialization and undercutting of European security.

This is in English, after Eugene Romer of Układ Sił media introduces me in Polish. This was at the “3 Seas -1 Opportunity Forum” in Gdansk, last June 4-5, 2024. I have been wanting to post it ever since, as the questions remain relevant. My thanks to Eugene and his team, and to his Opportunity Think Tank colleagues.

My panel at the forum was on problems of relying on energy security that arrives via the sea. So, think Poland and Lithuania’s LNG terminals, of the many sub-sea pipelines, power and communications cables between Baltic and Nordic states. And, since June, all the incidents where ships leaving Russian ports “accidentally” dragged their anchors, cutting such vital links. So, this conference was rather prescient. My sincere thanks to our hosts The Opportunity Institute for Foreign Affairs.

My long print interview at Lithuania’s LRT [Lithuanian PDF | English PDF] with Aleksandra Ketlerienė, deputy editor-in-chief of Lithuania’s LRT.lt, published 7January. We spoke in Warsaw, 19 November. My thanks to Aleksandra for her insightful questioning and editorial care. We discussed:

The EU’s systemic energy-policy “own goals” since its initial energy-crisis win after Moscow began cutting gas exports early in 2021.

Reforming failed/ineffective Russian price-cap sanctions for real sanctions, and how the global oil market is now favorable for “maximum pressure.”

Historical perspectives on oil, gas, renewables, and nuclear sectors, essential for realistic policy formation.

An historical overview of China’s decades-long effort to overcome its energy security, learning lessons of Japan’s WW2 weaknesses.

I appeared alongside Dr. Hashem Aqel, Oil and Energy Expert, Associate Fellow at Oxford Institute for Energy Studies, who contributed several insights. Asharq News is the Mideast Bloomberg partner. My further analysis follows:

Arabic, original broadcast version.

The recent rise in EU gas prices and the rapid depletion of what had been a significant surplus in EU storage, is principally a two-sided story.

One side is indeed about the impending cutoff of Russian gas, still flowing across Ukraine. This has been expected for months, and so is already largely priced in. Expectations of new transit across Ukraine of Russian-origin gas re-labelled as Azerbaijani was being negotiated. However, this deal fell apart, with the final nail in its coffin being when Ukraine’s President Zelensky asserted that Ukraine would not transit any further Russian-origin gas after 31 December unless payments to Russia are withheld until after the war ends. This seems a very reasonable demand for a country fighting for its survival against a Russian invasion. [See “Ukraine will not allow transit of Russian gas with Azeri label, Zelenskyy says, dashing Slovak hopes,” EuroNews, Jorge Liboreir 19 Dec. 2024.] This marks the end of the five-year contract, which was only agreed to at the last moment before New Year 2020, when the US Senate finally forced then-President Trump to agree to sanctions on Nord Stream 2 construction (I was in Kyiv, for Naftogaz, and on Ukrainian television, analyzing Washington sanctions, Kyiv-Moscow negotiations, and the pro-Nord Stream position of Berlin.)

The other side is a story of yet another European energy own-goal, a consequence of its over-reliance on weather-dependent renewable energy generation. This overreliance has made its electricity supply increasingly volatile, in sync with the weather. In November and early December, especially north and western Europe experienced what the Germans call “Dunkelflaute“, a protracted wind and solar drought. Batteries can only substitute for perhaps 40 minutes, or at best an hour. So, the de facto long-term, grid-scale “storage” backing up Europe’s plethora of wind and sun generation is really just natural-gas turbine electrical generation plants. The reality of increased generation (and hence, electricity market) volatility and dependence on gas backup generation was analyzed this week in a data-driven manner by the Oxford Institute for Energy Studies. [See: “Dunkelflaute: Driving Europe Gas Demand Volatility” Energy Insight: 161, by Anouk Honoré and Jack Sharples, Senior Research Fellows, OIES, 2024/12.]

I explain EU/German motives for seeking “green H2” import pipes, then (at time 11:30) questions I raised moderating at NAPEC re. EU-Algerian pipeline MOU.

Here’s my video from Oran, Algeria, after a very informative “Africa and Mediterranean Energy & Hydrogen Exhibition & Conference,” NAPEC 2024 (video highlights here). Two parts to my analysis:

First, (up to time 11:30) I explain the rationale and impetus for the EU drive for massive green hydrogen gas imports. This is primarily driven by Germany’s increasing desperation at being locked into over-reliance on weather-variable renewables, whose high prices are sparking its “deindustrialization,” especially after losing Russian gas pipeline imports due to Putin’s war on Ukraine, plus due to the own-goal shutting down of their zero-carbon, amortized (paid for) nuclear plants during the European energy crisis. (Note: I misspoke: “Grey” hydrogen would NOT have the CO2 stored, “Blue” would. Both are derived from natural gas.)

I also explain how this massive green hydrogen “fix” to “renewables fundamentalist” policy is a techno-panacea that simply cannot work. Then ..

ENGLISH Interview | Al Watan, Cairo. Thurs 10Oct24. 15 minutes

ARABIC Interview

At first, we focused on IEA warnings of a possible EU winder gas shortage due to supply-and-demand mismatches. I agree and expand on the IEA points.

Second, I explained that if Israel retaliates against Iran so strongly that it threatens the regimes survival, or is seen as intending to provoke regime change, then the Iranian leadership will have “nothing to lose” by in-turn escalating to the maximum. Aside from unleashing the maximum response of its proxies surrounding Israel, Tehran’s most potent weapon would be to spark a global oil and gas crisis.

Consider oil: Iran can either shut down the Straights of Hormuz (or simply make them unsafe for tankers) and/or, it can use missiles and drones to destroy significant parts of Saudi, UAE and other Gulf oil facilities, including perhaps even Azerbaijan’s as some Iranian propagandists have threatened.

Consider natural gas: Shutting the Straights or directly hitting Qatar’s massive LNG exports infrastructure would immediately stop Qatari LNG exports. As the world’s second largest LNG exporter, this would immediately cause a separate global natural gas crisis.

Berlin Energy Roudtable. L to R: Ben Aris, Tom O’Donnell, Morten Frisch & Andriy Kobolyev (video link from Kyiv) 24 October 2023, Haus der Bunderpresskonferenz – PHOTO GALLERY BELOW(Divan staff)

On 24 October, I was honored to moderate a great roundtable in Berlin with three European energy experts, sponsored by Der Divan Kulturehaus. SUGGESTION: While listening, open up that speaker’s file below. You’ll find Ben Aris’ data-slides on Russian price-cap failings, Andriy Kobolyev’s proposal to tax Moscow’s oil & Morten Frisch’s slides on EU renewable shortcomings & continued oil and gas needs.

You are invited to attend the 1st Berlin Energy Roundtable, on 24 October. Our three distinguished speakers share decades of Eurasian and Mideast gas-sector experience. I’ll have the pleasure of moderating.

As many of you know, this is a format I long sought to establish in Berlin; but, which during Corona and the energy-crisis after the largescale Russian invasion of Ukraine, was difficult to advance.

The event is made possible with the generous sponsorship of the Divan Culture Housein Berlin. Hopefully there will be several more in the coming year.