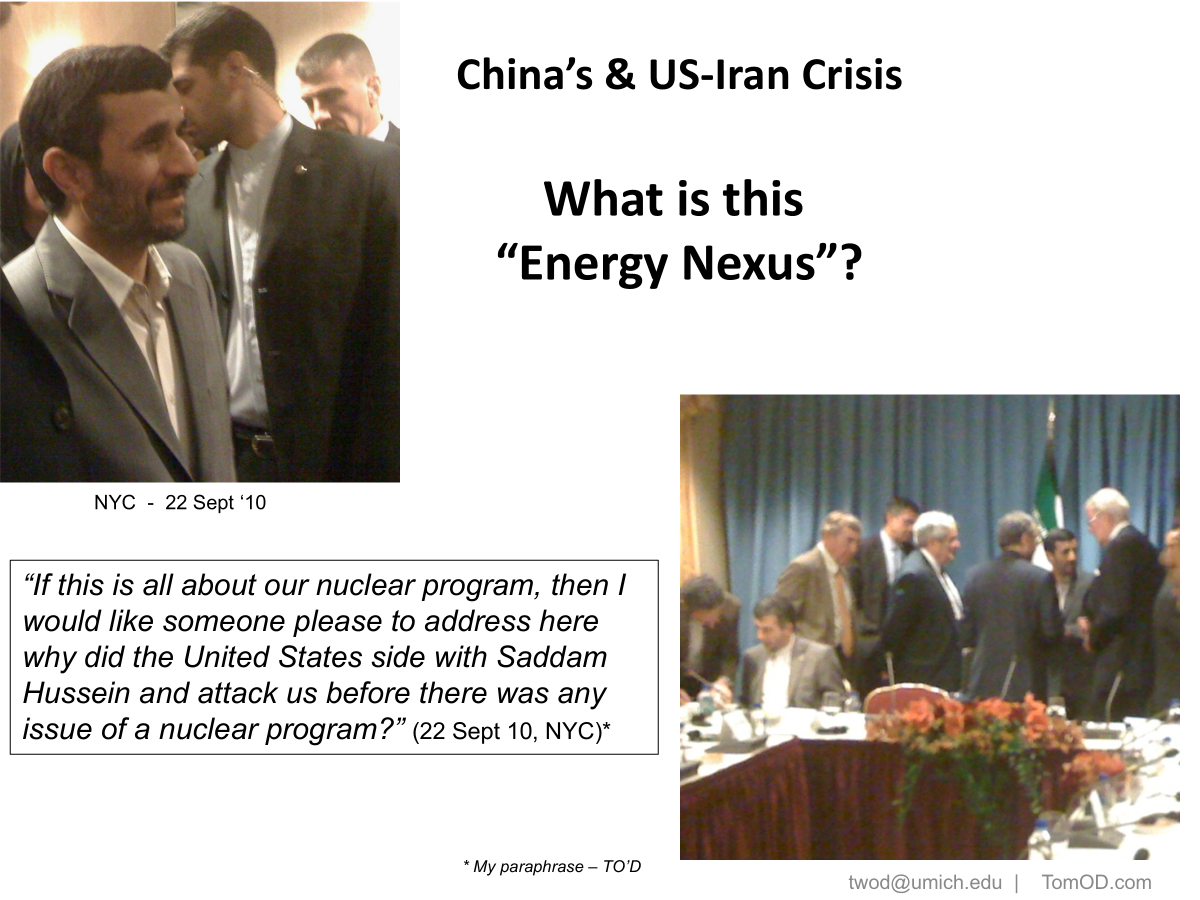

Some years ago, I was invited to dinner with President Ahmadinejad in NYC during the annual opening of the General Assembly.

The American think-tanks, consultancies, and x-diplomats present went on and on asking detailed questions about this or that scenario where US experts might work with Iranian experts to observe or limit the Iranian nuclear enrichment program. (I mentioned this 2010 dinner in a later post: “China’s Iran-Oil Import Angst. Part I” Feb 13, 2012.)

It became rather tiresome. Ahmadinejad clearly was growing tired of it. He then asked us,

“If this is all about our nuclear program, then I would like someone please to address here why did the United States side with Saddam Hussein and attack us before there was any issue of a nuclear program?” (Iranian President M. Ahmadinejad, 22 Sept 10, NYC, my notes, T.O’D.)

Everyone ignored his question, and simply kept up with their obviously pre-prepared technical questions. But, what had he meant?

To me, clearly he was referring to the Iran-Iraq war (Sept.1980-Aug.1988), when the USA, at a certain point, decided to take Iraq’s side and, among other things, sunk the entire Iranian Navy in a day, took over air traffic control for the Iraqi air force, started directly advising Iraq on strategy, and etc.

In the end, Iran had to accept an Iraqi peace deal after a crushing defeat facilitated by the USA. I recall now all these details vividly. And, all this was indeed well before any nuclear program.

Aside: I find it disturbing that so many “experts” refer to the supposed “Iraqi defeat” in that war. This was all understood at the time. For example, I quote here from the NYT, (Sec. A, Page 1, of July 21, 1988): Ayatollah Khomeini had personally endorsed the cease-fire demanded by United Nations Security Council Resolution 598. Iran’s supreme religious leader confirmed, for the first time, that he had approved the resolution and added, with his characteristic rhetorical flair: ”Taking this decision was more deadly than taking poison. I submitted myself to God’s will and drank this drink for his satisfaction.” (Emphasis added to the most famous part of Khomeni’s statement. T.O’D.) Further research will quickly show he had to sign as Iran was being soundly defeated at the time, hence the “poison” he had to swallow.

By the way, it is also known, at least in academic circles, from later extensive archival research, that the war with Iraq was planned and instigated by Iran, and that Iraq had attacked in response to Iranian provocations and signs of Tehran’s preparations, after warnings. I am happy to send references to those interested.

What I myself had been arguing, back then, during the Iran-Iraq War Ahmadinejad was referring to, was that the US-Iran confrontation was actually about the US opposition to any country, either from inside the Gulf Region or outside the Region, gaining hegemony over the Gulf and the Straits of Hormuz. This had to do with guaranteeing the free flow of oil, and that the global oil market would be a “real” market that no one state could unduly control. I had even coined a term, “The Global Barrel,” for this market-centered, post-OPEC-nationalizations collective oil-security system, a system initiated by Henry Kissinger in 1973.

Continue reading

00

00 Here`s my latest at Berlin Policy Journal: about OPEC`s 30 Novermber meeting, US shale and the geopolitics from the Trump Administration towards Iran and the Saudis. – Tom O`D.

Here`s my latest at Berlin Policy Journal: about OPEC`s 30 Novermber meeting, US shale and the geopolitics from the Trump Administration towards Iran and the Saudis. – Tom O`D.

This Wikistrat Report on the Saudi kingdom’s “reform” plans and the future of oil is from a press webinar I did on 17 May together with Dr. Ariel Cohen (Atlantic Council, Washington) and Prof. Shaul Mishal (Middle East Division, IDC Herzliya & Tel Aviv U.). A nicely done report on oil market and geopolitical hot topics.

This Wikistrat Report on the Saudi kingdom’s “reform” plans and the future of oil is from a press webinar I did on 17 May together with Dr. Ariel Cohen (Atlantic Council, Washington) and Prof. Shaul Mishal (Middle East Division, IDC Herzliya & Tel Aviv U.). A nicely done report on oil market and geopolitical hot topics.